A significant one-time credit arising from reorganization gains and “fresh-start accounting” valuation adjustments resulted in third quarter net earnings of $655.7 million for Catalyst Paper. The company emerged from creditor protection on September 13, 2012 with significant debt and cost-structure improvements.

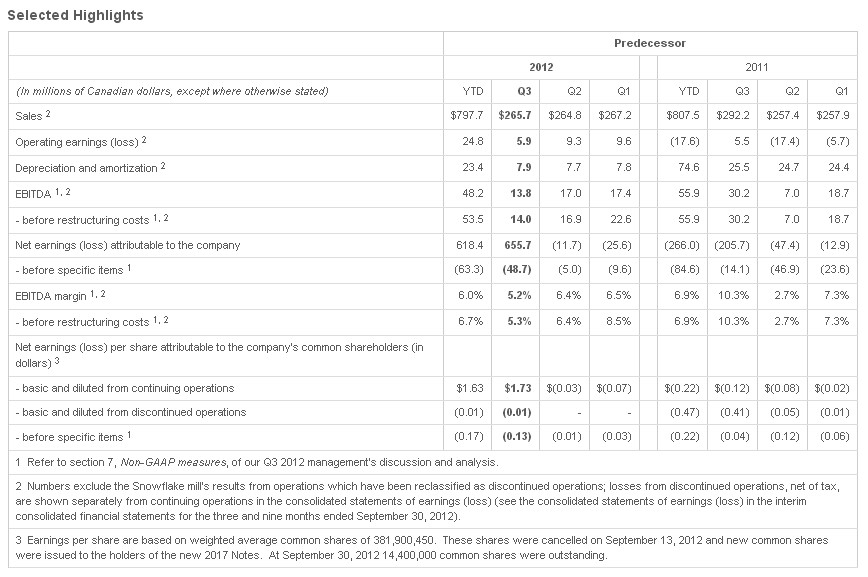

Net earnings this quarter contrast with a net loss of $11.7 million the quarter before. Sales were essentially unchanged at $265.7 million. The net after-tax restructuring-related credit was $688.1million. An after-tax foreign exchange gain on translation of U.S. dollar denominated debt of $25.2 million further supported Q3 earnings.

Before these and other specific items, Catalyst posted a net loss for the third quarter of $48.7 million, compared to a net loss of $5.0 million in the prior quarter. Earnings before interest, tax, depreciation and amortization (EBITDA) in the third quarter were $13.8 million and EBITDA before restructuring costs was $14.0 million, compared with EBITDA of $17.0 million and EBITDA before restructuring costs of $16.9 million in the second quarter.

“The third quarter marked a turning point for Catalyst as we exited creditor protection with a stronger balance sheet, lower interest costs and lower annual operating costs going forward,” said President and CEO Kevin J. Clarke. “This puts us on stronger operational footing to address ongoing market dynamics. And it means Catalyst can now take a much more active role in the transformation of the industry as a whole.”

Creditor Protection and Restructuring Process

After filing for creditor protection on January 31, 2012, Catalyst secured 99% approval from voting creditors for its second amended plan of arrangement under the CCAA on June 25, 2012. The plan subsequently received court sanction in British Columbia and was confirmed by the US Court in Delaware. A new asset-based loan (ABL) facility was in place on September 13, 2012, meeting the final pre-condition for implementation of the plan.

Previous secured note holders received shares and US $250 million of new senior secured notes due 2017 in exchange for their US$390 million of secured notes due 2016. In addition, we issued US$35 million of new exit notes under a secured exit financing facility on September 13, 2012, to pay restructuring costs and expenses and to manage other contingencies on exit from CCAA protection.

The restructuring has reduced Catalyst’s debt by $390 million, eliminated $80 million of accrued interest, and reduced annual interest expense and other cash costs by $70 million.

Catalyst’s operations are continuing in substantially the same form, and a new board of directors took office upon exit from CCAA. Previous secured note holders now own all of the 14.4 million new common shares that are presently issued and outstanding. An addition of approximately 135,000 common shares will be issued to unsecured creditors who made an equity election in respect of their claims under the plan. Additional shares may be issued under a new management incentive plan that may be adopted in future. An application has been submitted to the Toronto Stock Exchange for a public listing of the new common shares.

Fresh start accounting has been applied as of September 30, 2012, in accordance with U.S. Generally Accepted Accounting Principles. This involved use of independent financial advice to determine an enterprise value for the company and the fair value of Catalyst’s assets and liabilities.

Snowflake Closure

The previously announced permanent closure of the Snowflake mill in Arizona, which primarily manufactured recycled newsprint, was implemented on September 30, 2012. This will stem operating losses and reduce annualized selling, general and administrative expenses. A court-approved sales process for the mill and associated assets was announced on September 17, 2012.

The closure is expected to result in one-time cost of approximately $9.7 million ($8.7 million of which had been paid or accrued by quarter-end) and ongoing costs of approximately $0.6 million per month until disposition. These costs are expected to be largely recouped by sales proceeds.

Performance and Market Overview

Operating earnings of $5.9 million were up from the same quarter last year and on a year-to-date basis but lagged Q2 operating earnings of $9.3 million. They were negatively impacted by reduced pulp transaction prices, a stronger Canadian dollar, increased power costs, and a pulp inventory write-down. Offsetting factors included higher overall sales volumes, lower maintenance costs and lower labour costs – the final factor being an outcome of new collective agreements reached during the restructuring.

North American demand was down year-over-year across specialty paper product lines – most notably by 18.0% for uncoated grades and by 15.4% for directory. Benchmark prices were up moderately for coated grades from the second quarter, but unchanged for other specialty products. Sales volumes decreased while average sales revenue remained flat year-over-year.

North American newsprint demand saw a marginal 1.4% year-over-year increase, although the average benchmark price dropped from the second quarter due to marketplace inventory buildup. Sales volumes increased while average sales revenue was down year-over-year.

Markets for Northern Bleached Softwood Kraft pulp remained weak as a result of end-user inventory in China, and the benchmark price for that market dropped by 8.7% from the second quarter. There were year-over-year declines in both sales volumes and average sales revenue.

Liquidity

Quarter-end liquidity of $96.8 million was down from $125.9 million a year prior, but up from $71.8 million at the end of the second quarter due to a larger borrowing base under the new ABL facility. Cash on hand was down mainly due to payment of success fees of $6.9 million on emergence from creditor protection and debt issuance costs of $9.3 million.

(click picture to enlarge)

Outlook

The U.S. economic recovery in the first half of 2012 moderated somewhat though employment data, housing and financial markets held steady. The Canadian dollar remains near par and currency volatility is expected to ease somewhat through year-end and early 2013.

Specialty printing paper markets will be positively affected by seasonally strong demand in the fourth quarter. Producer and consumer inventories are relatively low with good industry operating rates for most specialty grades, especially coated and high gloss. Price increases for coated grades announced for October 1st are expected to be partially implemented though the Port Hawkesbury mill restart will make seasonally slow specialty markets even more challenging in the first quarter of 2013.

Newsprint demand is expected to decline modestly through the remainder of the year and exports are likely to remain sluggish. However, the Snowflake mill closure has tightened operating rates in the West and prices are expected to increase marginally in our freight-logical markets while remaining flat in Eastern markets.

Demand for NBSK pulp is expected to increase slightly in the fourth quarter driven primarily by China. Prices are expected to recover from the lows they reached in the third quarter. Further price appreciation is dependent on global demand and supply dynamics and growth in Chinese consumption.

On the operations side, price pressure is expected to ease on fibre and some chemicals. Maintenance costs are expected to increase with two boiler outages and a scheduled 12-day outage on one of our pulp lines and recovery boilers. Crofton No. 1 paper machine will continue to be indefinitely curtailed for the foreseeable future.

Capital spending in 2012 is forecasted to be approximately $25 million, and energy efficiency projects funded through the Federal Green Transformation Program are complete and on track to deliver EBITDA in excess of $5.0 million in 2012.

Further Quarterly Results Materials

This release, along with the full quarterly report (Management Discussion &Analysis, Financial Statements and accompanying notes) are available at www.catalystpaper.com/Investors. This material is also filed with SEDAR in Canada and EDGAR in the United States.

Kevin J. Clarke, president and CEO, and Brian Baarda, vice-president finance and CFO, will hold a conference call on Wednesday November 14, 2012, at 11 a.m. ET, 8 a.m. PT to present the company’s third quarter results. Financial analysts and institutional investors are invited to dial 1-888-231-8191 (North America) or 1-647-427-7450 (Toronto / International) reservation number 56717173#. Media and other interested people may join the live webcast in listen-only mode at www.catalystpaper.com